Monday BS #17: 07.02.22

On money

If you’re interested in why people do what they do, why your partner leaves clothes lying around the bathroom floor or what makes your clients tick, then you should subscribe to Monday BS newsletters and A Load of BS podcasts for limitless entertainment and self-improvement.

What’s the value of money?

When it comes to money, we make absurd decisions about how to spend it all the time. Whether this is buying a £3.50 latte at Starbucks while we price compare groceries to save 10 pence on apples, bolting on a ‘special’ car cleaning kit for £250 after spending £15,000 on a new vehicle, or hopelessly overbidding on eBay auctions because we already feel attached to the item in question, we are irrational, emotional and flawed creatures. How on earth are we supposed to value things?

Such mental accounting may be economically sub-optimal, but it makes our worlds go round. There simply isn’t enough time in the day (nor inclination) to calculate the opportunity cost of every transaction we make. So we take shortcuts, make contradictions and fall into cognitive booby traps. There is good sense in this sometimes.

“Cogito, ergo non sum homo economicus.”1

We talk frequently of increasing financial literacy as the panacea for our spending and saving ills. I’m not sure education of this kind is the answer, because most of us, regardless of our means, are aware of our own temptations for immediate gratification or for twisted, creative accounting narratives for buying the £100 bottle of wine that would have Enron purring.

Jeff Kreisler and Dan Ariely wrote Small Change: Money Mishaps and How to Avoid Them about these very questions, about our inability to value things, how we cope in this sea of uncertainty and ignorance and how to overcome biases that the best of us are susceptible to.

I’m interviewing Jeff soon for A Load of BS so we’ll have time to delve into these conundrums more. Indeed, if you’ve just splashed out on a 417 ft yacht and feel you’ve pushed the boat out (or is that the other Jeff?) or less outlandishly feel that you’re dining out spending is out of control, then feel free to share your questions for Jeff (Kreisler) in the comments below, and I’ll credit you in the show.

Getting on with our lives

There is no silver bullet to financial sanity, but a mix of well intentioned and structured financial services and our own proactivity can make a huge difference. Here are three thoughts.

Helpful nudges

Intermittent indulgence

Stop and think

Helpful nudges

Nudges come from the outside, altering people's behaviour in a particular direction by encouraging positive choices rather than restricting unwanted behaviours.

To get around our weakness for spending today rather than putting a few bob aside for a rainy day, Shlomo Benartzi and Richard Thaler pioneered Save More Tomorrow, a program to make saving for retirement as easy and painless as possible. By showing employees long-term rates of return rather than short-term ones, their willingness to invest more of their retirement savings in stocks increased.

Since 2006, over 15m Americans have benefited from this nudge. Indeed, as digital banking becomes ever more normalised, algorithms can notify customers automatically when their account balances drop below predefined levels, which customers can set for themselves (opt in) or which banks can set for them (opt out).

Getting even more personal to support customer wellbeing, neo bank Monzo introduced an optional gambling block to prevent customers using their cards with gambling operators. This is now expanded to all Monzo’s Open Banking partners meaning the block extends beyond use of just the Monzo card. This nudge is based on research carried out by The Behavioural Insights Team.

Much nudging is about reducing friction in customer experience, often luring us into psychological traps to spend more without feeling the pain of paying - I present Apple Pay M’lud. In the gambling case, very cleverly, friction and pain are being deliberately reintroduced.

Intermittent indulgence

Back to that £100 bottle of wine. Most of the time, we buy wine at home for £8-12 a bottle. As wine expert Joe Fattorini told me on our podcast, there isn’t much quality return on a bottle beyond £30, after which we’re entering Veblen goods territory. But on occasion, we want to indulge and have a stupidly expensive drink; we want a maximising experience, not a satisficing one. There is pleasure rather than pain in splurging and the cocktail of status and scarcity is intoxicating before a glass has been poured. This is no time for a logical value analysis.

Keeping it liquid, Richard Thaler conducted research on the very subjective, non-econ ways in which we value wine. Another reminder that we don’t always do what’s best for us! Take a look and decide where you stand.

The broader point I want to make here on indulgence is that an over precise, over-mechanised, black or white approach to monetary value, one without nuance, colour or imagination is a sad place, and one that we shouldn’t strive for at all costs.

With our obsession for machine intelligence, we are on a one way track to decontextualized ways of thinking. It’s of course in our gift to put the brakes on and embrace the rough edges where we can afford to.

Accepting for context, life is bland without the odd treat.

Stop and think

Pausing over every latte purchase to consider preferable alternatives to your £3.50 of hard earned money is not good advice. But if there are areas of your finances which are pushing you into the red or endangering your longer-term ambitions, take a time out every few months, check yourself, accept your illogical tendencies and take simple actions to keep yourself on track. There’s no great science in that.

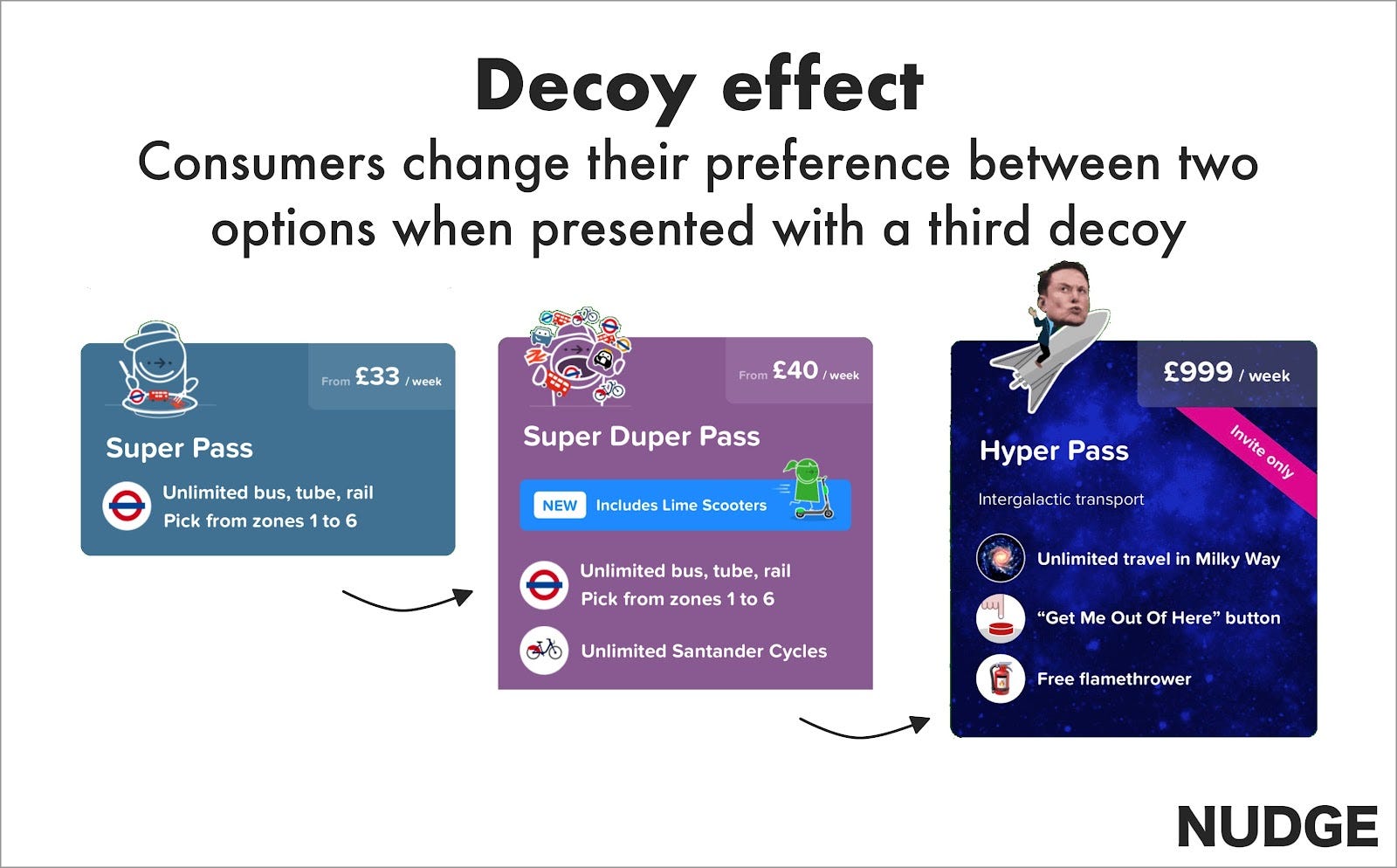

With that in mind, here comes a nifty piece of BS from my friend Phill Agnew which retailers pull on us all the time, the decoy effect. Now you’ll be armed to avoid its trap.

Guest contribution from Phill Agnew

Phill's an aspiring behavioural scientist who'll try anything to broaden his understanding. He once told 5,000 people not to listen to his podcast to test out this nudge (spoiler alert, it resulted in Nudge Podcast's highest number of daily downloads).

The decoy effect is a simple bias.

Buying decisions change when consumers are presented with a third decoy choice.

Here’s an example.

Say you go to the cinema and you see two choices for popcorn:

Some people will pick large, some will pick medium. It's probably a fairly even split.

But say you add a decoy.

An XL version that's considerably more expensive:

It’s £3 more. But only one size up.

Now, most will pick large.

Why?

Because the XL decoy makes the large price look like a better deal.

Only 50p more than medium, yet £3 cheaper than XL.

This isn't hearsay. It's proven in multiple studies by Dan Ariely.

It’s been used to boost Economist subscriptions and it’s why McDonald’s offer a Signature Range.

But here's my favourite example from CityMapper:

It's a parody of course.

Obviously, they won't send you a flamethrower or provide intergalactic transport.

In fact, you can't even buy it. It's invite-only.

Yet, I reckon it works. More people probably buy the middle Super Duper Pass because of it.

Phill’s focus on Nudge Podcast is the application of behaviorial science to marketing. He has loads of great guests (like the inimitable Rory Sutherland, Richard Shotton and Vanessa Bohns) who share actionable tips you can apply.

If you’d like more BS

You can find all my podcasts here on Substack or Apple, Spotify et al. So tune in to hear more from me and Jeff Kreisler on the value of money as well as other stories.

Have a great week!

Daniel

Daniel & Descartes

What a great post - thank you! A question for Jeff Kreisler: How can we use uncertain but positive outcomes - including prize draws and lotteries - to maximise public good and personal utility?