Coming out of the Shadows: FinTech on Paths Less Trodden (Part 2)

The new frontiers for financial access and inclusion

Welcome to all new readers of the Paths Less Trodden interview series. Join other smart, curious folks by subscribing here:

Paths Less Trodden is brought to you by Tshepo, one of South Africa’s most exciting and sought after fashion brands.

Tshepo Mohlala’s story, values and life philosophy are a perfect match for everything that I am striving to show in this newsletter. From the most humble beginnings, Tshepo (meaning hope), the self-taught stylist and designer, has built his business from the ground up, and is recognised as one of South Africa’s hippest denim brands.

He is a born fighter and entrepreneur of the best kind. Follow his rise to international stardom on Twitter and Instagram. Or follow the celebrities and taste makers who love him by checking out the beautiful Presidential Slim Fit jeans here.

Hi friends 😀,

In part 1 of my interview with Carlos Alonso Torras of FinTech Collective, published on Tuesday, I set the scene for FinTech activity, trends and challenges in Latin America and Africa. In this follow-up, I’d like to share thoughts on underdog bets, where next in LATAM (or not), the global picture (who will grasp the nettle?), the less obvious potential of crypto, building ecosystems and sustaining the momentum.

Let’s pick up where we left off. Carlos emphasised that when FinTech Collective is looking at new hubs, they’re thinking more about Africa than Latin America…

Coming out of the Shadows Part 2

It’s the future, but not as we know it

The underdog bet

Away from the buzz around Nigeria, East and Southern Africa, I believe Ethiopia is one of the next frontier African bets.

Driving through Addis Ababa, you literally inhale the change and development in front of your eyes.

With the second largest (and young) population in Africa at 114m and fast GDP growth in the last 15 years (average 10% annually), Ethiopia can build on early start-up foundations like the country’s first accelerator, Iceaddis. To progress, they must build more tech infrastructure (talent pathways, facilities, access to capital). For now, real estate prices are high and entrepreneurship is treated with more suspicion than admiration. If the country can regain its pre-COVID mojo, during which growth dropped from 8.14% in 2109 to 6.1% in 2020, this is one to watch.

Where next in LATAM?

The question of where next in LATAM is also not straightforward. Carlos quickly knocks over my hypothesis for Argentina and Chile as heirs apparent. “Argentina has a lot of talent, especially on the DeFi [decentralised finance] side; but the whole market is small. And the country, macroeconomically and regulation wise, is extremely difficult. Mercado Libre [e-commerce marketplaces and online auctions] became massive because they left Argentina. Ualá [personal financial management mobile app] did well in Argentina but moved to Mexico.”

“Chile is probably the most developed market in LATAM but it’s very small. You’re going to have to look outside to grow; Columbia and Mexico are usually the markets that Chilean companies look at.”

Mexico City, Sao Paulo and Bogota are clearly where the action is. Elsewhere, for now, are springboards and test beds for bigger ambition.

The bigger picture

The financially underserved of course spread far beyond FinTech Collective’s investment memos. Financial inclusion (having a bank, savings and transaction account) is one of the UN’s sustainable development goals because, according to the World Bank, still 1/3 (1.7bn) of adults globally remain unbanked. That’s roughly 25% LATAM, 25% Africa and 50% Asia. Paradoxically, countries who often top the unbanked list have quite developed banking systems (as defined by account penetration); but there is still a high percentage of unbanked who are costly to service and so overlooked. China is the prime example with an 80% rate of inclusion but top of the unbanked population list at 225m. Not uniquely, they have a large rural population which is unattractive for commercial banks.

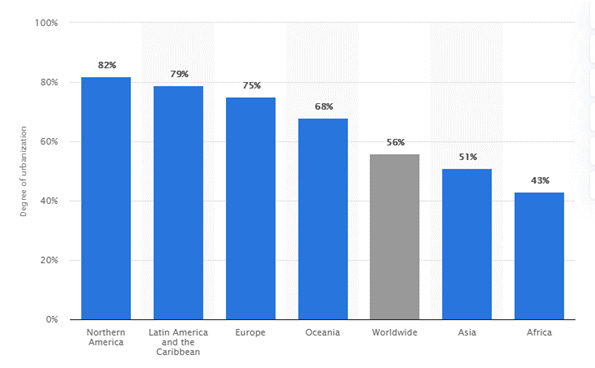

Degree of urbanization (% of urban population in total population) by continent in 2020

Carlos reminds me that the picture is very different in Asia and Africa vs. LATAM and so entrepreneurial focus is inevitably also different: “LATAM is the second most urbanised region in the world where close to 80% of the population live in big cities.”

“Take Mexico as a target market, you look at Mexico City, then you look at Monterey, you look at Guadalajara, and if you capture those three markets, you've already scaled to an insane amount.”

“Similar in Brazil, you look at Sao Paulo, you have Rio, Belo Horizonte, then Curitiba. From a cost effectiveness standpoint, it's unlikely entrepreneurs are going to prioritise rural areas.” Division of wealth and access to finance between rural and urban areas remain a concern, an area Carlos would encourage public sector and government to be more active in in collaboration with the private sector. With a long way still to go, Chinese financial reforms have pulled MSEs (micro and small enterprises) and the agricultural sector out of poverty. According to the People’s Bank of China (PBC) and the China Banking and Insurance Regulatory Commission (CBIRC), by the end of June 2020, outstanding loans to MSEs and agricultural areas in China reached RMB40.7 trillion (USD40.7 tr) and RMB37.8 trillion (USD5.9 tr), accounting for 24% and 22% respectively of the total outstanding loans of financial institutions.

Whether in China or Brazil, emerging market banks have historically focused on large corporations and state owned enterprises (SOE). While tension between State and Internet vibrates strongest in China, they cannot ignore the value of technology and private enterprise. Or I should say they shouldn’t ignore it. The sad dismembering of Jack Ma’s Alibaba empire now underway in China is a depressing Putin/Mugabe like déjà vu asset reallocation, or ‘rectification’ in Beijing language. Term it as you like, but this is retrogressive value destruction of the worst kind. Read George Calhoun’s Forbes article on this ‘strategic blunder on China’s part’.

Brazil has been more forthcoming and, beyond its commitment to open banking, the Banco Central do Brasil six months ago launched Pix, an instant payment system to send or receive payments in seconds. India’s government too has restructured its financial landscape to encourage a shift from cash to digital, eradicating corruption and promoting healthy and sustainable development along the way.

India has standout characteristics which heighten its FinTech potential – 400m newly connected people in the last four years by Reliance Jio, and its strength in developing software engineering talent; beyond those repatriating from the US, this is a heritage LATAM does not possess.

Could the future be crypto?

Projecting into the future, once whole populations are connected and we all carry a computer in our hands, there will likely be a more level playing field between developing and developed markets in terms of access to finance. No bad thing if this also heralds the end of the developed vs. developing market categorisation, considered already lazy, overly colloquial and outdated by some, based as it is on 1960s measures of infant birth and mortality rates. Bill Gates and Hans Rosling — author of the book ‘Factfulness’ (which I highly recommend) — have used a new categorical system; four distinct income levels that are now recognized as a more accurate way to describe countries and the range between them.

Balaji Srinivasan, formerly CTO at Coinbase and a General Partner at venture capital firm Andreessen Horowitz, presents a far more radical future where territories are defined by conventional capitalism (US), communism (China) and crypto (which he would call international capitalism). Crypto is the next technology paradigm up for grabs and in terms of creating greater liquidity in financial services, this is an opportunity for ‘developing’ markets to steal a march on the so called developed markets in FinTech.

LATAM is ahead of the game versus the US in some aspects anyway (e.g. the PIX central bank payment system in Brazil); wire transactions in US still take days and are expensive. With crypto, all you need is an Ethereum address, the ultimate common language. Could India, or perhaps Brazil, step forward to become a crypto capital as a symbol of transparent digital finance, a freedom to transact with whomever you want?

The moment for crypto here seems to me quite different, more fundamental from the froth and speculation we’re seeing in the US and Europe now. Regardless of the current popularity of Bitcoin or Ethereum and the underlying programmatic potential of blockchains, the opportunity to shift the predominant digital coin use case from store of value, greed and wealth creation to a transparent, low friction digital currency to enable the new, connected middle-classes in micro-transactions and skill building is an exciting one.

Particularly in countries with volatile currencies exacerbated by COVID devaluations (who also can’t rely on USD – step forward, for example, Venezuela), slow money movement systems and high levels of banking concentration, crypto plus connectivity allows millions to do remote jobs from their phones and move money peer to peer quickly. Carlos puts it neatly: “Philosophically speaking, decentralised finance appeals to people whose experience of finance is overly centralised and has failed them to some degree.” As an aside, in the face of the crypto onslaught, Simon Taylor at 11:FS has written a thought provoking piece on today’s generation of FinTechs suffering from the same innovators’ dilemma that the banks fell into 10 years ago. In parallel, Packy McCormick addresses this Web3 threat to disrupt the Web 2.0 tech giants in ‘Who Disrupts the Disrupters?’. Go deeper and listen to a16z partner Chris Dixon on crypto meaning and potential on the ‘Invest Like the Best’ podcast.

The leapfrog question

While crypto and Blockchain may hail a democratising force for finance (think a globally operable Mpesa), start-ups from the emerging world are already leapfrogging the US and teaching it a few things. Despite Silicon Valley’s arrogance, TikTok shows that a social network can function outside of US rules. When we think of open finance, the most sophisticated exemplars are far from home, like embedded finance super-app Go-Jek in Indonesia, superseding US or European FinTech ecosystems in terms of breadth of services. Colombian headquartered multi-vertical Rappi is another good example.

I should highlight Credit Karma in the US (and UK now) who used the credit record as a wedge into customers’ financial lives. Adding value fast, they have built a most virtuous flywheel for growth, layering on new services as they build trust, loyalty and a database.

Credit Karma Flywheel

1.5m members trusted Credit Karma to file their taxes in 2019. 10m+ members have turned to them for ID monitoring and they are now all things for your car: valuation, loans, recalls, insurance. 10m members are using this service. They have since moved into home services and money management. The business has over 100m members, counts over 50% of all US millennials as customers and was acquired by Intuit in December 2020 for $8.1bn cash and stock. Enough said.

Crossing borders, Stripe’s acquisition of Paystack however adds real validation to the potential of newer markets to create leading, multi-dimensional companies. Large corporations like Mastercard, Visa and Google are focusing too now on Africa, LATAM and Asia to invest and help develop tech talent. It still though remains a hurdle to identify and encourage new, young entrepreneurs to risk more stable income to start new businesses, to take a path less trodden.

Factories of talent

As the sophistication grows, we are starting to observe organic market regeneration as first wave start-up successes like 99Taxis (acquired by Didi), NuBank, the Brazilian digital bank with 40m customers, and Creditas, the largest FinTech in Brazil offering secured loans, have spawned new businesses started by departing battle-hardened talent or have invested in new ones, either by freshly minted founders or through corporate M&A.

NuBank has just raised another $750m to fuel growth in Brazil and Mexico, $500m of which is from Warren Buffet’s Berkshire Hathaway. This is a flying endorsement of the digital challenger banks generally, and of Brazil FinTech specifically. Their approach mirrors Credit Karma. This is another ecosystem done well – first the credit card, then a bank account, then access to investing. The more of a customer’s financial life they can own, the better they can monetise it, add more layers, rebundle services.

As Carlos puts it, “concentric circles are built around the initial stories.” Both PagSeguro and Stone (digital payment services for businesses) from Brazil IPO’ed in New York in 2018. This momentum is giving market liquidity, promoting ecosystem thinking, meaning start-ups are crossing borders and forming partnerships more fluently. Mexican digital gig worker services platform Heru partnered with Uber Eats recently. PayJoy started in Mexico offering micro-loans and is now serving the US with offices in San Francisco (as well as China, India and South Africa). N.B. this geographical transfer is typically harder the other way around as the operating costs of a US provider make them less affordable in LATAM.

Mexico in particular is seeing repatriation of talent; Mexicans who have MBAs or top degrees from the US are coming home to work on ambitious, exciting projects. There is also local recycling, Carlos cites Uber as a great example from where top notch talent is feeding back into start-ups. “If young entrepreneurs can see a path to success, examples of success, they see resources around them, incubators and accelerators that can help them get there, then that changes things, it makes it more tangible and realistic. If you look especially at Brazil, the amount of active early stage funds, accelerators and incubators in the ecosystem is impressive. So the path to get there is ready. It's been proven.”

The paths to get there are indeed ready, but to twist a quote from Simon Taylor at 11:FS, “FinTech is only 1% finished.” In 5-10 years time however, we hope that everyone has access to high quality, affordable financial products, that banking is far more global in nature and indeed the barriers to launch new kinds of products is even lower.